In today’s fast-paced digital world, understanding the intricacies of online transactions is more important than ever, especially for businesses looking to thrive in the e-commerce landscape. If you’ve ever wondered about the roles of payment gateways and payment processors, you’re not alone! While these terms are often used interchangeably, they serve distinct functions that can significantly impact your business’s bottom line. Choosing the right solution can enhance customer experience, streamline transactions, and ultimately drive sales. In this article, we’ll break down the crucial differences between a payment gateway and a payment processor, helping you make an informed decision for your business. So, let’s dive in and unravel the complexities of these two essential components of online payments!

Exploring the Basics of Payment Gateways and Payment Processors

When it comes to processing payments online, payment gateways and payment processors are often mentioned in the same breath, but they serve distinct roles in the transaction ecosystem. Understanding the difference between these two components is crucial for businesses looking to optimize their online sales strategy. While they work together to facilitate transactions, each has a unique function that contributes to a seamless payment experience.

A payment gateway acts as the intermediary that securely transmits payment information from a customer to the payment processor. It encrypts sensitive data, such as credit card numbers, ensuring that it is transmitted safely over the internet. This layer of security is vital, as it protects both the customer and the merchant from potential fraud. Without a reliable payment gateway, the risk of data breaches increases significantly, making it a critical component for any online business.

On the other hand, a payment processor is responsible for handling the actual transaction. Once the payment gateway captures the customer’s information, the processor takes over to verify the transaction and facilitate the transfer of funds from the customer’s bank to the merchant’s account. This stage involves communication with various financial institutions, ensuring that all parties involved in the transaction are properly authenticated.

Here’s a quick comparison to illustrate their distinct functions:

| Feature | Payment Gateway | Payment Processor |

|---|---|---|

| Primary Function | Securely transmits payment data | Handles transaction approval and fund transfer |

| Security Role | Encrypts sensitive information | Validates and processes payment |

| Integration | Works with online stores to collect payments | Connects with banks and financial institutions |

It’s also worth noting that many merchants opt for bundled services that include both a payment gateway and a payment processor, simplifying the integration process and offering a more streamlined solution. By using a single provider for both services, businesses can reduce compatibility issues and improve their overall transaction efficiency.

understanding the differences between payment gateways and payment processors is essential for any business engaged in e-commerce. By leveraging the strengths of both components, merchants can create a secure and efficient payment experience that encourages customer trust and promotes sales growth.

Understanding the Roles: How Payment Gateways and Processors Work Together

When it comes to online transactions, understanding the distinction between payment gateways and payment processors is crucial for anyone looking to set up an e-commerce business. While they are often used interchangeably, these two components serve different purposes and work in tandem to ensure smooth and secure transactions for both merchants and customers.

A payment gateway acts as the intermediary between a customer’s bank and the merchant’s bank. It is responsible for securely capturing and encrypting the customer’s payment information, such as credit card details, before transmitting it to the payment processor. Essentially, think of the payment gateway as the digital equivalent of a point-of-sale terminal. It not only facilitates the transaction process but also ensures that sensitive information is protected throughout the transaction. Key features of a payment gateway include:

- Encryption to secure sensitive data

- Fraud detection tools to minimize risks

- User-friendly interfaces for seamless checkout experiences

On the other hand, a payment processor takes on the role of managing the transaction after the payment gateway has done its job. Once the gateway has securely captured payment information, the processor handles the actual transaction by communicating with the customer’s bank to transfer funds to the merchant’s account. This process involves several steps, which may include authorization, settlement, and funding. Here are some of the core functions of a payment processor:

- Authorization to confirm sufficient funds

- Settlement to process and transfer funds to the merchant

- Reporting for tracking transaction history and analytics

| Feature | Payment Gateway | Payment Processor |

|---|---|---|

| Transaction Security | ✔️ | ✔️ |

| Fund Transfer | ❌ | ✔️ |

| User Interface | ✔️ | ❌ |

| Analytics | ❌ | ✔️ |

while the payment gateway and payment processor may seem like two sides of the same coin, they each play distinct and critical roles in the transaction process. By understanding how they work together, businesses can choose the right solutions to meet their needs and provide a secure, seamless experience for customers.

Key Differences Between Payment Gateways and Payment Processors

When navigating the world of online transactions, it’s crucial to understand the distinct roles that payment gateways and payment processors play. Although they often work together seamlessly, they serve different purposes in the payment ecosystem.

Payment Gateways act as the virtual equivalent of a point-of-sale terminal in a physical store. They securely capture and transmit customer payment information to the payment processor. Here are some key characteristics:

- Security: They encrypt sensitive information, ensuring that data passes securely between the customer and merchant.

- User Experience: They provide a user-friendly interface for customers to enter their payment details.

- Integration: Most gateways can easily integrate with websites and shopping carts, streamlining the customer checkout experience.

On the other hand, Payment Processors are the behind-the-scenes players that handle the actual transaction. They are responsible for transferring funds from the customer’s bank to the merchant’s account. Here’s what sets them apart:

- Transaction Handling: They manage the processing of payments, including authorization and settlement.

- Financial Relationships: Payment processors work with banks to facilitate the transfer of funds.

- Fees: They often charge transaction fees, which can vary based on volume and payment methods.

To illustrate their differences clearly, consider the following table:

| Feature | Payment Gateway | Payment Processor |

|---|---|---|

| Function | Captures & encrypts payment data | Transfers funds between banks |

| User Interaction | Visible to customers | Behind the scenes |

| Security Focus | High | Moderate |

understanding the differences between these two components is essential for any business owner looking to set up a robust payment solution. Recognizing their unique roles can help you choose the right tools for your business needs, ensuring a smooth and secure payment experience for your customers.

Choosing the Right Solution: Factors to Consider for Your Business

When it comes to accepting payments for your business, understanding the differences between a payment gateway and a payment processor is crucial. Choosing the right solution can significantly impact your transaction experience, customer satisfaction, and, ultimately, your bottom line. Here are some essential factors to consider:

- Transaction Volume: Assess your business’s transaction volume. A high volume may necessitate a more robust payment processor that offers competitive pricing structures and lower transaction fees.

- Type of Business: Consider whether you operate online, in-person, or both. This will influence whether you need a payment gateway, a processor, or a combination of both.

- Integration Ease: Ensure that the solution you select integrates seamlessly with your existing systems, such as your eCommerce platform or accounting software. A complicated setup can lead to unnecessary delays.

- Security Features: The safety of your customers’ payment information is paramount. Look for solutions that offer advanced security features like encryption and fraud detection.

- Customer Support: Choose a provider known for reliable customer support. In the event of an issue, prompt assistance can make all the difference in maintaining your business operations.

| Feature | Payment Gateway | Payment Processor |

|---|---|---|

| Functionality | Authorizes payments | Manages funds transfer |

| Setup Complexity | Usually simpler | Can be complex |

| Cost Structure | May have monthly fees | Typically per transaction fees |

| Security | SSL and encryption | PCI compliance |

Ultimately, the decision should align with your business goals, customer expectations, and operational capabilities. Taking the time to evaluate these factors will empower you to select a solution that not only meets your current needs but also grows with you. Remember, investing in the right payment infrastructure is not just a choice; it’s a strategic move towards enhancing your business efficiency and customer trust.

Cost Considerations: Unpacking Fees Associated with Gateways and Processors

When diving into the world of payment gateways and processors, one of the most crucial aspects to consider is the cost structure. Understanding the fees associated with each service can significantly impact your business’s bottom line, especially if you’re processing a high volume of transactions. Let’s break down some of the common fees you might encounter.

Payment gateways typically charge the following fees:

- Setup Fee: A one-time fee for integrating the gateway with your online store.

- Monthly Fee: A recurring fee that covers the maintenance of the gateway.

- Transaction Fee: A fee charged for each transaction processed through the gateway.

- Chargeback Fee: A fee applied when a customer disputes a transaction.

On the other hand, payment processors also have their own set of fees, which may include:

- Discount Rate: A percentage of each transaction taken as a fee.

- Transaction Fee: Similar to gateways, processors charge a fee per transaction.

- Monthly Fee: This may apply for account maintenance and support.

- Batch Fee: A fee for settling daily transactions, often charged per batch.

To give you a clearer picture, here’s a quick comparison of typical fees:

| Fee Type | Payment Gateway | Payment Processor |

|---|---|---|

| Setup Fee | $0 – $500 | $0 – $100 |

| Monthly Fee | $10 – $30 | $0 – $25 |

| Transaction Fee | $0.10 – $0.30 + % | 2.5% – 3.5% |

| Chargeback Fee | $15 – $25 | $20 – $50 |

Keep in mind that while lower fees may seem appealing, the overall functionality and service quality of a payment gateway or processor are equally important. A slightly higher fee might be worthwhile if it comes with superior customer support or enhanced security features. Always consider the total cost of ownership instead of just the upfront fees.

Lastly, don’t forget to read the fine print! Fees can vary based on your business model, transaction volume, and even the industry you’re in. Taking the time to thoroughly assess and compare different options ensures you choose a solution that aligns not just with your technical needs but also with your financial strategy.

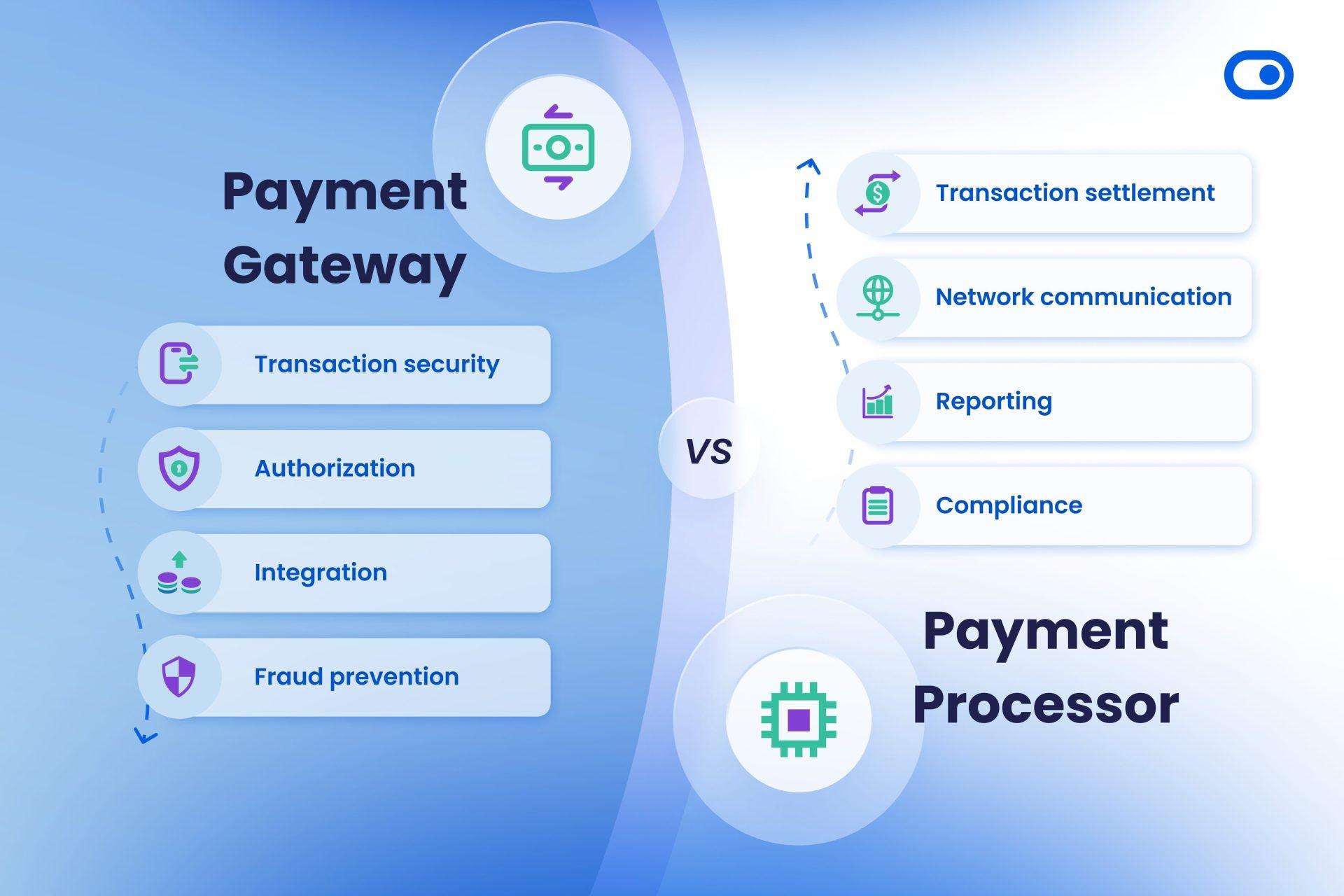

Security Matters: How Each Option Protects Sensitive Information

When it comes to safeguarding sensitive information in online transactions, understanding the distinct roles of payment gateways and payment processors is essential. Each option brings its own set of security features designed to protect both consumers and merchants from potential threats.

Payment Gateways: These serve as the first line of defense. They are responsible for encrypting sensitive information, such as credit card numbers, during transactions. This encryption ensures that even if data is intercepted, it remains unreadable. Key security features of payment gateways include:

- SSL Certificates: Secure Sockets Layer (SSL) technology establishes a secure connection between the user’s browser and the server, shielding data from eavesdroppers.

- Tokenization: This replaces sensitive card information with a unique identifier or token, reducing the likelihood of data theft.

- Fraud Detection Tools: Advanced algorithms monitor transactions in real-time, flagging any suspicious activities for further verification.

Payment Processors: While they handle the transactions themselves, their security measures also play a crucial role. Payment processors are responsible for the actual transfer of funds between the customer’s bank and the merchant’s account. Their security protocols typically include:

- PCI Compliance: Adhering to the Payment Card Industry Data Security Standard (PCI DSS) ensures that processors meet rigorous security requirements.

- Data Encryption: Just like gateways, processors utilize encryption to protect data during transfer, adding an additional layer of security.

- Chargeback Protection: They help manage disputes and chargebacks, offering merchants additional security against fraudulent claims.

When evaluating security, it’s vital for businesses to consider how these two components work together. By implementing a robust payment gateway paired with a trustworthy payment processor, merchants can create a stronghold against potential security breaches. Here’s a quick comparison:

| Feature | Payment Gateway | Payment Processor |

|---|---|---|

| Data Encryption | ✔️ | ✔️ |

| Tokenization | ✔️ | ❌ |

| PCI Compliance | ✔️ | ✔️ |

| Fraud Detection | ✔️ | ✔️ |

| Chargeback Management | ❌ | ✔️ |

both payment gateways and payment processors play vital roles in the secure handling of sensitive information during online transactions. By choosing options that prioritize security, businesses can not only protect their customers but also enhance their own reputation in a competitive market.

User Experience: Streamlining Checkout for Your Customers

When it comes to optimizing the checkout experience, understanding the differences between a payment gateway and a payment processor is crucial. Both play essential roles in facilitating online transactions, yet they serve distinct functions that can impact the overall user experience and streamline the checkout process for your customers.

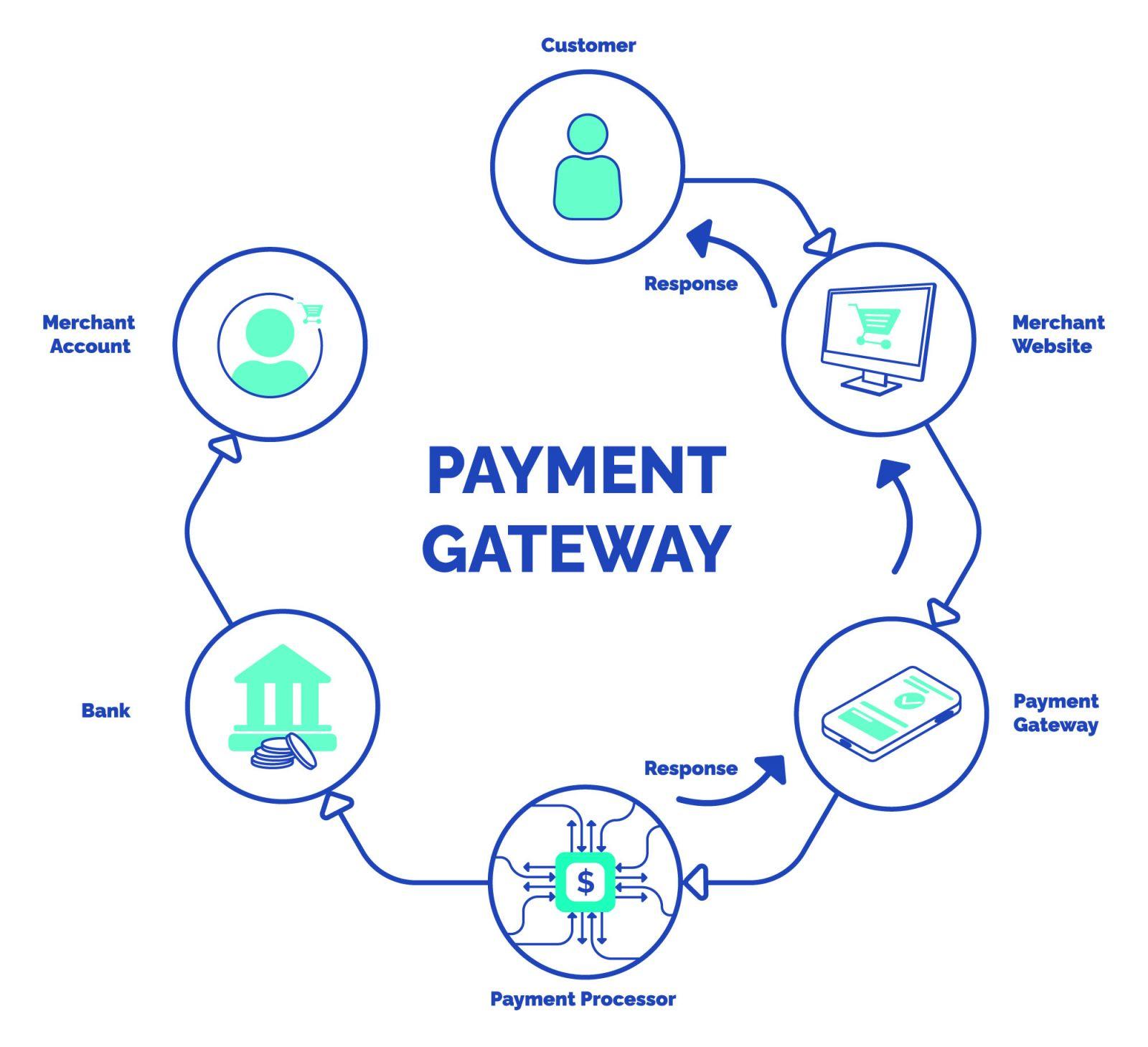

A payment gateway acts as the digital equivalent of a point-of-sale terminal in a brick-and-mortar store. It securely captures and transmits the customer’s payment information to the processor. Here are some key features of a payment gateway:

- Encrypts sensitive customer data for security

- Facilitates various payment methods (credit cards, digital wallets, etc.)

- Provides a seamless user interface for customers during checkout

On the other hand, a payment processor is responsible for handling the transaction itself. After the payment gateway collects and encrypts the customer’s details, the processor verifies and completes the transaction with the bank or card network. Understanding these distinctions can help you choose the right tools for your business:

| Payment Gateway | Payment Processor |

|---|---|

| Captures payment information | Handles the transaction |

| Provides front-end integration | Works behind the scenes |

| Ensures data security | Communicates with banks |

Choosing the right payment gateway and processor can significantly enhance the user experience. Opt for a solution that allows quick and easy setup, offers responsive support, and integrates seamlessly with your e-commerce platform. A streamlined checkout process not only reduces cart abandonment rates but also fosters customer trust and loyalty.

understanding the interplay between these two components will empower you to create a smooth and efficient checkout experience. Prioritize options that align with your customer’s needs and preferences, ensuring that each transaction feels secure and hassle-free. The right combination can lead to higher conversion rates and satisfied customers who return to shop again.

Integrating Payment Solutions: What You Need to Know

When it comes to online transactions, understanding the roles of different players in the payment ecosystem is crucial for any business owner. While the terms payment gateway and payment processor are often used interchangeably, they serve distinct functions that are vital for successful payment integration. Knowing the differences between these two can help you make informed choices that enhance your customers’ experience and your operational efficiency.

A payment gateway is essentially the digital equivalent of a point-of-sale terminal located in physical retail locations. It acts as a bridge between the customer and the payment processor. When a customer makes a purchase online, the payment gateway encrypts sensitive information, such as credit card numbers, to ensure that the data is transmitted securely. This layer of security is essential, especially in today’s digital landscape where online fraud is a growing concern. Key features of a payment gateway include:

- Encryption: Protects sensitive information during transactions.

- Integration: Easily connects with various e-commerce platforms.

- Customer Interface: Provides a streamlined checkout process for users.

On the other hand, a payment processor handles the transaction once it has been initiated. After the payment gateway captures the payment information, it is the payment processor’s job to facilitate the transaction with the customer’s bank and the merchant’s bank. This process involves verifying the transaction details and transferring funds. Some important aspects of a payment processor include:

- Transaction Management: Manages all facets of the transaction process.

- Settlement: Ensures funds are moved from the customer’s account to the merchant’s account.

- Reporting: Provides detailed transaction reports for financial tracking.

| Feature | Payment Gateway | Payment Processor |

|---|---|---|

| Function | Secure transaction data | Facilitate fund transfer |

| Security | Encrypts customer data | Ensures transaction authorization |

| User Interaction | Interface for checkout | Backend transaction handling |

Both payment gateways and processors are essential for e-commerce operations, and understanding their differences can lead to better decision-making for your payment solutions. By integrating both effectively, you can not only provide a secure and seamless shopping experience for your customers but also streamline your business operations. When evaluating payment options, consider how each component complements your goals and customer needs.

Future Trends in Payment Processing: What to Expect Ahead

As we look to the future, the landscape of payment processing is poised for significant transformation. One of the most prominent trends is the rise of contactless payments, driven by the growing demand for convenience and safety. As consumers increasingly prefer quick and secure transactions, businesses will need to adapt to this shift by integrating contactless options into their payment systems.

Another exciting development is the adoption of blockchain technology within payment processing. This innovation promises to enhance security, reduce transaction fees, and streamline cross-border payments. By utilizing decentralized ledgers, businesses can not only speed up their transactions but also build consumer trust through transparency, a critical factor in today’s digital economy.

Furthermore, the advancement of artificial intelligence (AI) and machine learning will revolutionize how transactions are processed. These technologies can analyze transaction patterns to detect fraud in real-time, offering a dual benefit of heightened security and improved customer experience. As fraud becomes more sophisticated, AI tools will be essential in safeguarding sensitive information and ensuring seamless transactions.

Lastly, we cannot overlook the increasing importance of mobile wallets. As more consumers turn to their smartphones for everyday purchases, businesses will need to ensure their payment gateways support mobile wallet integration. This trend not only caters to consumer preferences but also enhances loyalty by offering convenience and personalized experiences.

| Trend | Description |

|---|---|

| Contactless Payments | Fast and safe transactions with no physical contact. |

| Blockchain Technology | Enhanced security and lower fees through decentralized systems. |

| AI & Machine Learning | Real-time fraud detection and improved transaction efficiency. |

| Mobile Wallets | Convenient payment solutions that enhance customer loyalty. |

Making the Right Choice: A Quick Guide to Selecting a Payment Solution

Choosing the right payment solution can significantly impact your business’s success. With a variety of options available, understanding the distinction between a payment gateway and a payment processor is essential for making an informed choice. Here’s a breakdown to help you navigate these critical components of online transactions.

Understanding Payment Gateways

A payment gateway acts as the first line of communication between your business and the customers. It securely captures and transfers the payment information from the customer to the processor. Here are some key features of payment gateways:

- Security: They encrypt sensitive data, ensuring safe transactions.

- User Experience: Often designed to integrate seamlessly into your website for a smooth checkout.

- Payment Methods: Support various payment methods, including credit cards, digital wallets, and more.

Delving into Payment Processors

On the other hand, a payment processor is responsible for handling the transactions once the payment information is received. This includes verifying and authorizing the funds. Here’s what you should know:

- Transaction Management: They manage all aspects of the transaction, including transfers of funds.

- Merchant Account: Typically, a payment processor requires a merchant account to deposit funds.

- Fee Structures: Fees can vary based on the processor and transaction volume, impacting your overall costs.

Key Differences at a Glance

| Feature | Payment Gateway | Payment Processor |

|---|---|---|

| Function | Captures and encrypts payment info | Processes the actual transaction |

| Security | Provides encryption and fraud protection | Manages transaction security and compliance |

| User Interaction | Visible to customers during checkout | Behind-the-scenes operation |

Choosing What Suits Your Business

Ultimately, the best solution depends on your specific business needs. If you want a solution that focuses on customer interaction and security, a robust payment gateway might be your priority. Conversely, if you require a reliable mechanism for transaction management and fund transfers, selecting an effective payment processor is essential. Consider your business model, expected transaction volume, and customer preferences when making this crucial decision.

Frequently Asked Questions (FAQ)

Q&A: Payment Gateway vs. Payment Processor: What Are the Differences?

Q1: What exactly is a payment gateway?

A1: Great question! A payment gateway is like the digital equivalent of a point-of-sale terminal you see in a store. It securely authorizes credit card payments and processes transactions between the customer and the merchant. Think of it as the bridge that connects your online store to the financial institutions that handle your payments. It encrypts sensitive information, ensuring that your customers’ payment details are kept safe while they complete their purchases.

Q2: And what about a payment processor? How does that fit in?

A2: A payment processor is a bit different but equally essential. While the payment gateway handles the front end—meaning it communicates with your customers— the payment processor works on the back end. It takes the transaction data from the payment gateway and interacts with the bank to complete the sale. Essentially, the processor is responsible for moving the money from the customer’s bank to your account. Without it, the transaction wouldn’t be complete!

Q3: Are they the same thing? Can I use one without the other?

A3: Not quite! While they often work together and are sometimes bundled into one service, they fulfill different roles. You can technically use a payment processor without a payment gateway if you’re handling payments in-person, but for online transactions, you’ll need both to ensure a seamless, secure experience for your customers. It’s like trying to drive a car without wheels—you won’t get very far!

Q4: Why does it matter to understand the difference?

A4: Understanding the difference is crucial for any business owner! Choosing the right services can impact your transaction fees, customer experience, and overall security. If you know what you need, you can select the best solutions that align with your business model. Plus, having this knowledge can help you negotiate better rates and terms with providers. It’s all about empowerment!

Q5: What should I consider when choosing a payment gateway and processor?

A5: Look for flexibility, security, and integration. You want a payment gateway and processor that can easily integrate with your existing systems, support multiple payment methods, and provide robust security features, like encryption and fraud detection. Also, consider transaction fees! Every penny counts, especially for small businesses.

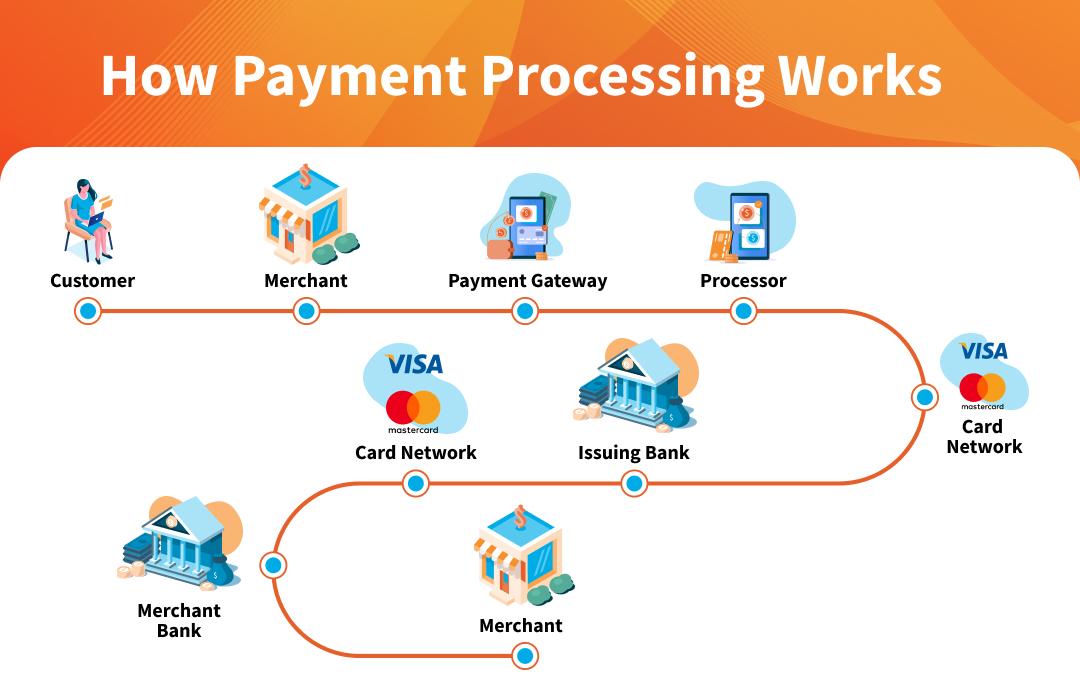

Q6: Can you give an example of how they work together in a transaction?

A6: Absolutely! Let’s say a customer wants to buy a pair of shoes from your online store. They enter their credit card details on your website (the payment gateway). The gateway encrypts that info and sends it to the payment processor. The processor then contacts the customer’s bank to verify the funds and approves the transaction. Once approved, the money moves from the customer’s account to your account, and the payment gateway sends a confirmation back to your website. Voila! Transaction completed!

Q7: Any final thoughts for businesses deciding between options?

A7: Yes, take your time to research! Don’t just go with the first option you find. Read reviews, compare features, and think about your business’s future needs. A good payment gateway and processor can make all the difference in providing a smooth customer experience and streamlining your operations. Remember, happy customers make for a successful business!

Concluding Remarks

understanding the differences between payment gateways and payment processors is crucial for anyone navigating the world of online transactions. While they work hand in hand to ensure seamless payment experiences, each plays a distinct role that can significantly impact your business operations. By choosing the right tools, you can enhance your customer experience, streamline transactions, and ultimately drive sales.

So, whether you’re an established business owner or just starting out, take the time to evaluate your options. Consider how each component fits into your overall strategy and choose the solution that aligns with your goals. Remember, a well-informed decision today can lead to greater success tomorrow.

Don’t hesitate to explore further, ask questions, and reach out for expert advice. The right payment infrastructure can make all the difference in your journey to financial success. Happy transacting!